The appraisal is one of those steps in a real estate deal that many buyers and sellers find confusing, yet it’s also one of the most critical.

To put its importance into perspective, every year, licensed appraisers complete millions of evaluations across the U.S. (NAR data suggests roughly 13 million residential appraisals annually), which gives lenders, buyers, and sellers a realistic view of current market value.

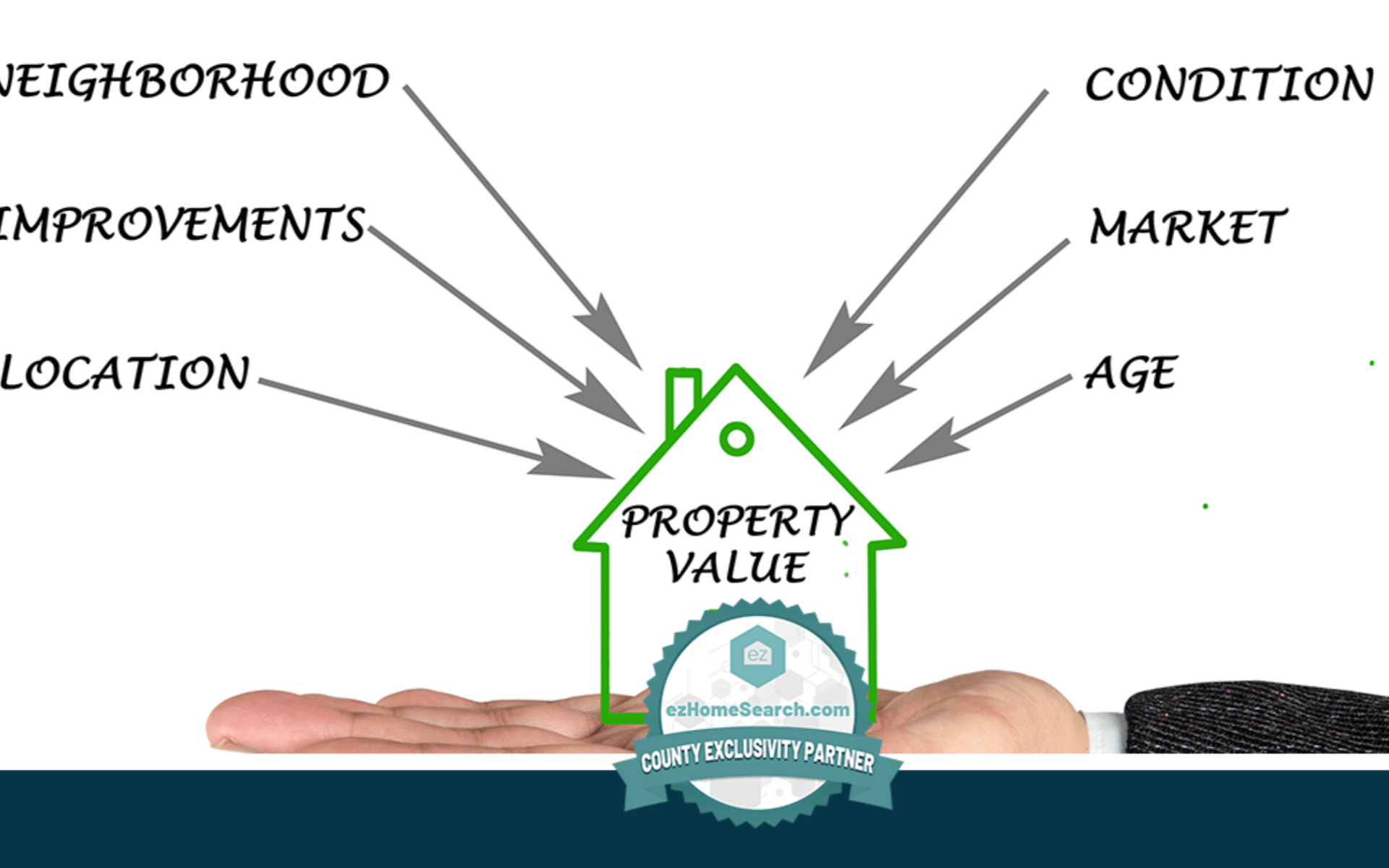

That might sound intimidating, but the process is structured and based on facts, such as recent sales, property condition, upgrades, and square footage, all of which play a role in the final number.

You’ll see exactly how the appraisal works, what the appraiser actually checks, and what it means for you if the value comes in a little higher or lower, so you feel clear, informed, and ready to take the next step without second-guessing anything.

What Is a Home Appraisal and Why Does It Matter

Put simply, a home appraisal is a certified appraiser’s evaluation of what a property is worth in today’s real estate market. Unlike a guess or a quick online estimate, it’s based on strict state and federal guidelines (USPAP) and real market data.

Appraisers look at the home’s size, condition, location, upgrades, and recent sales nearby to arrive at a fair number.

A home appraisal is a crucial part of any real estate transaction because lenders want assurance that the property is worth the amount they’re financing.

- For buyers, an appraisal helps avoid overpaying for a home.

- For sellers, it backs up their asking price and reduces the risk of a deal falling through.

Home Appraisal vs. Home Inspection

It’s super common to confuse an appraisal with a home inspection. However, they’re not the same thing at all. Think of it this way:

- The appraisal is about money and value. The appraiser’s job is to figure out what the home is worth in the current market. They’ll measure the square footage, look at upgrades, note the lot size, and compare it against recent sales in the neighborhood. Their report tells the bank, “Yes, this property supports the loan amount.”

- The inspection is about the condition. An inspector isn’t worried about market value. Instead, they’re crawling into attics, checking the foundation, testing electrical systems, and making sure there aren’t hidden issues that could turn into expensive headaches later.

Both steps matter when you’re buying or selling a home. The appraisal protects the lender by making sure they don’t lend more than the house is worth, but it also protects you from overpaying. The inspection, on the other hand, protects you as the buyer, giving you a clearer picture of what you’re actually moving into.

Together, both processes provide everyone involved a sense of security: you know what you’re paying for, the seller knows their price is supported, and the lender knows the loan makes sense.

Why Lenders Require a Home Appraisal

Lenders don’t approve loans on trust alone; they want proof. An appraisal confirms the home is worth the loan amount, protecting the bank if the borrower defaults. Without this step, lenders could end up financing more than a home could actually sell for.

For buyers, this safeguard means you won’t borrow more than the property’s value. For sellers, it means your home’s price is supported by data, which helps keep the deal on track.

Step-by-Step Guide to the Home Appraisal Process

Ready to discover how home appraisals work? Here’s a step-by-step look at the home appraisal process, so you’ll know exactly what to expect from the moment it’s ordered to the day the report lands in your hands.

Step 1: The Appraisal Is Ordered

The appraisal process starts within a few days of the seller accepting your offer. Although the buyer is the one who pays the fee (that often ranges between $300 and $500, sometimes higher for unique or complex properties), the lender is the party that orders the appraisal.

This setup isn’t accidental. After the 2008 housing crisis, federal reforms required lenders to oversee the process to prevent inflated valuations and protect against biased reporting. In practice, that means neither the buyer, the seller, nor the real estate agents involved can hand-pick an appraiser.

Instead, lenders usually assign appraisers through an Appraisal Management Company (AMC) or a regulated rotation system. Every appraiser must hold a state license or certification and follow the Uniform Standards of Professional Appraisal Practice (USPAP).

That independence is what makes the report credible and why banks are willing to rely on it when approving large loans.

For buyers, this step may feel frustrating: you pay the bill but don’t get to choose who shows up. Still, it’s also your safeguard. And insurance that the appraisal ensures you’re not borrowing more than the home is truly worth.

For sellers, the appraisal can be reassuring if it supports the agreed price, but it can also be a pivotal moment if the value comes in low, forcing tough negotiations. Either way, this early step sets the tone for how smoothly the rest of the transaction moves toward closing.

Step 2: The Appraiser Begins Market Research

Before ever walking through the door, an appraiser begins with a thorough market analysis. This isn’t the same as the Comparative Market Analysis (CMA) that real estate agents prepare. A CMA is a helpful pricing tool, but it’s informal. An appraiser’s market analysis is regulated, tied to lending standards, and far more comprehensive.

The backbone of this stage is identifying comparable sales (also known as “comps”). These are recently sold homes that mirror the subject property in square footage, layout, condition, and location.

Appraisers rely on sales from the past three to six months within about a one-mile radius. When data is scarce, they’ll expand the timeline or search area to find the best available matches. Once selected, comps are carefully adjusted for differences.

For instance, a home with an extra half-bathroom, a renovated kitchen, or a larger lot won’t be treated as an equal match to one without those features. Each adjustment narrows in on fair market value.

But the process doesn’t stop there. Appraisers also complete a Market Conditions Analysis, a deeper look at what’s happening across the neighborhood and beyond. This includes:

- Price trends: Are property values rising, steady, or showing signs of decline?

- Absorption rate: How quickly is the current inventory selling?

- Days on market: Are homes moving in a week or sitting for months?

- Supply and demand balance: Is limited inventory fueling bidding wars, or is buyer activity slowing down?

- Local influences: Job growth, interest rate shifts, or seasonal patterns that affect buyer demand.

By blending comparable sales with market-wide indicators, the appraiser develops a data-driven expectation of value before the inspection. When they finally step inside the property, the on-site visit either confirms the picture or reveals details the numbers alone couldn’t capture.

Step 3: The Appraiser Conducts an On-Site Inspection

After building a market framework, the appraiser visits the property in person. This inspection is not as exhaustive as a home inspection, but it’s detailed enough to verify the property’s condition, features, and overall appeal. The goal is to see how the home stacks up against the comparable sales already researched.

What the appraiser looks at:

- Exterior: Curb appeal, lot size, landscaping, roof condition, driveway, garage, and structural soundness. They also check the property’s setting –is it on a busy road, near a park, or overlooking water? Location nuances can influence value.

- Interior: Square footage, layout, number of bedrooms and bathrooms, and overall condition. Appraisers note upgrades (like renovated kitchens or bathrooms), quality of finishes, flooring, appliances, and any functional issues such as awkward floor plans or poor lighting.

- Condition: General upkeep matters. Deferred maintenance (peeling paint, outdated systems, visible cracks) can drag down value, while well-kept homes support higher estimates.

- Improvements & Additions: Documented renovations, additions, or energy-efficient upgrades may add measurable value, especially if supported by permits and receipts.

- Health and Safety Factors: While not a full inspection, appraisers flag items that could affect livability or financing, like missing handrails, water damage, or broken windows. For FHA, VA, or USDA loans, they must also confirm the property meets specific safety and livability standards, which can make this review stricter than for conventional loans.

Documentation Collected

Appraisers take photographs of the exterior, major interior spaces, and any items that could influence value positively or negatively.

They also prepare a floor plan sketch to verify square footage and layout. These materials, along with their notes, become part of the official appraisal report.

Alternative Appraisal Formats

Not every appraisal involves a full interior and exterior review. Lenders sometimes use faster, limited options in certain situations:

- Drive-by appraisals rely on an exterior inspection, supported by public records and listing data.

- Desktop appraisals are completed entirely off-site, using MLS data, tax records, and third-party information.

These options are less detailed and generally reserved for low-risk loans or refinancing.

The on-site inspection ensures the appraisal isn’t just numbers on a page. Two homes with identical square footage may be valued very differently if one has been updated and the other shows signs of neglect. By capturing these differences firsthand, the appraiser validates the market data and refines the property’s value.

The inspection itself can take anywhere from 30 minutes for a condo to a few hours for a large or custom home. Once complete, the appraiser returns to their research and analysis, blending these findings with the market study to determine the final value.

Step 4: Analysis and Valuation

Once the inspection is complete, the appraiser pulls everything together:

- The market data.

- The property details.

- Their observations from the visit.

All of that collected data is used to determine a credible market value for the home. This stage happens back at the desk, where numbers meet judgment.

The sales comparison approach is the backbone of most residential appraisals. The appraiser studies comps and adjusts them for differences.

A comp with a larger lot or a finished basement will be adjusted down to match the subject home, while a property without the upgrades your home offers will be adjusted upward. But numbers only go so far.

The home’s condition, layout, and livability often tip the scale. Two houses with the same square footage may differ in value by tens of thousands of dollars if one is updated and the other shows signs of neglect.

Alternative Approaches

While comps are primary, appraisers may also consider other methods:

- Cost approach: Estimates what it would take to rebuild the home today, minus depreciation, plus land value. This is often used for new builds or unique homes.

- Income approach: Relevant for rental or multi-family properties, where value is tied to income potential.

Even if these approaches aren’t central in a single-family appraisal, appraisers reconcile all available data to ensure the final number makes sense

Limits of Adjustments

Adjustments can’t cure everything. A remodeled kitchen or new roof adds value, but no upgrade can fully offset being located on a noisy highway or next to industrial land. Location and market realities still hold the most weight.

The Role of Documentation

Every conclusion must be defensible. That’s why appraisers include photographs of the home’s interior and exterior, floorplan sketches, and notes on upgrades or deficiencies. These become part of the official appraisal report, ensuring the valuation isn’t just an opinion but a documented, reviewable record.

The final figure is not an average, but a reconciled opinion of value that lenders rely on to approve financing. It determines the loan-to-value ratio (LTV), which can make or break a deal.

For buyers, it’s reassurance that the price they’re paying lines up with the market. For sellers, it’s the validation that keeps a contract moving forward.

Once the analysis is complete, the appraiser delivers their findings in an unbiased written report known as the appraisal report. The document lenders, buyers, and sellers will all look to as the official word on the property’s value.

Step 5: The Appraisal Report Is Delivered

Once the on-site inspection and analysis are complete, the appraiser compiles everything into a formal report. For most residential loans, this takes the form of the Uniform Residential Appraisal Report (URAR, Form 1004), which is the industry standard.

The report is detailed, covering:

- Property specifics: location, lot size, square footage, features, and condition.

- Comparable sales and adjustments: how recent sales were chosen and where value differences were added or subtracted.

- Market data and commentary: notes on broader trends that shaped the conclusion.

- Exhibits: maps, photos, floorplan sketches, and other documentation that validate the findings.

Reports vary in length depending on the property and required exhibits, but they are often extensive, combining the form itself with maps, photos, and addenda.

Who Gets the Appraisal Report?

The appraisal is delivered directly to the lender, not the buyer or seller. This preserves independence under federal Appraiser Independence Requirements (AIR).

However, under the Equal Credit Opportunity Act’s Valuations Rule, buyers are entitled to a copy promptly upon completion or at least three business days before closing. Sellers don’t have a guaranteed right to see it; they only gain access if the buyer or contract terms provide for sharing.

Interpreting the Conclusion

The appraiser’s value opinion reflects fair market value as of the effective date of the report. While many buyers focus solely on the final figure, it’s worth reviewing how the comps and adjustments align with the property’s condition. Those details reveal why the number landed where it did.

What Happens If the Appraisal Comes in Lower or Higher Than the Offer Price

An appraisal can swing the outcome of your home purchase. Sometimes it’s smooth sailing, other times it introduces new hurdles. Here’s how the different scenarios play out:

If the Value Matches or Exceeds the Offer

This is the ideal situation. If the appraisal comes in at or above the contract price:

- Lender approval is smooth. The loan amount is supported.

- Buyer peace of mind. You’re not overpaying.

- Seller confidence. Independent data validates your asking price.

At this point, most transactions move forward without a hitch.

If the Value Comes in Low

This is where things get tricky. A low appraisal means the lender won’t finance the full contract price, leaving a gap. Common ways buyers and sellers handle it include:

- Renegotiating the price: The seller may agree to lower the price closer to the appraised value.

- Splitting the difference: Both sides compromise, adjusting the sale price so the buyer covers part of the shortfall in cash.

- Buyer makes up the gap: The buyer brings additional funds to closing to cover what the loan won’t.

Can You Request a Second Appraisal?

If you believe the appraisal is flawed, you can challenge it through a reconsideration of the value request. This usually involves providing:

- Better or more recent comparable sales.

- Documentation of overlooked upgrades or features.

- Evidence of errors in the report (like missed square footage or incorrect data).

The lender reviews the request and decides whether to have the appraiser revise the report. While not always successful, a strong rebuttal can raise the value.

How to Prepare for a Home Appraisal

Whether you’re selling or buying, a little preparation can make the appraisal process smoother, and in some cases, help secure a stronger valuation. See below how each side can approach it.

Tips for Sellers Preparing for a Home Appraisal

The appraiser is walking in with data already in hand, but presentation and documentation still matter. A few smart steps can help your home put its best foot forward:

- Handle minor repairs: Fix leaky faucets, cracked tiles, loose handrails, or peeling paint. Small issues can make a home look less cared for.

- Freshen up curb appeal: Trim landscaping, clear pathways, and tidy up the exterior. First impressions influence how your home is perceived against the comps.

- Highlight upgrades with proof: Gather permits, receipts, and warranties for renovations or additions. Documented improvements carry more weight than verbal claims.

- Make every space accessible: Unlock basements, attics, garages, or sheds. If the appraiser can’t see it, it won’t be factored in.

- Point out neighborhood benefits: Share recent improvements nearby, like a new park, school renovations, or infrastructure upgrades. Appraisers don’t always have the latest local intel.

- Be present but not pushy: You can be home, but give the appraiser space. A simple handoff of your documentation is far more effective than hovering.

Tips for Buyers Preparing for a Home Appraisal

You can’t control the inspection, but you can prepare for its implications and how it affects your financing.

- Budget for the fee upfront: Expect to pay between $300 and $600 for an appraisal on most homes. Larger and unique types of properties frequently have higher costs. Lenders often require this payment before the assessment takes place, so be ready.

- Understand the timeline: Appraisals are usually ordered within days of the offer being accepted, and results often take about a week. Knowing this keeps closing expectations realistic.

- Check credentials: Confirm through your lender that the appraiser is state-certified and familiar with your market. Local expertise matters for an accurate valuation.

- Review key documents: Familiarize yourself with your loan estimate and appraisal requirements, so you know how the result affects your financing.

- Know your options if issues arise: If the appraisal comes in lower than expected, you and your agent can request a “Reconsideration of Value” by submitting stronger comparable sales.

Frequently Asked Questions About Home Appraisals

What Do Appraisers Look for During a Home Appraisal?

Appraisers evaluate both the interior and exterior of the house, looking well beyond surface impressions. Inside, they consider measurable factors such as square footage, bedroom and bathroom count, and how functional the layout is for everyday living.

They also note the home’s overall condition, whether systems and finishes are modern or dated, and give weight to upgrades like remodeled kitchens, energy-efficient windows, or finished basements. On the exterior, curb appeal, structural integrity, lot size, landscaping, and even the surrounding street environment play a role.

Outside, appraisers take in the full picture of the property. They evaluate curb appeal (how attractive and well-kept the home looks from the street) along with the size and usability of the lot, roof condition, and landscaping quality.

Structural elements like the driveway, foundation, siding, and garage also factor into the assessment. Just as important is the setting: is the home on a quiet cul-de-sac, a busy street, or backing up to a park or lake? Location nuances can significantly influence desirability and, therefore, value.

To anchor these observations, the appraiser compares your home to recent sales of similar properties in the neighborhood, adjusting for differences in size, condition, and features to reach a fair market value.

Outside, they consider curb appeal, lot size, roof condition, landscaping, and the overall setting. They also compare your home to recent sales of similar properties in the area.

How Can I Increase My Home’s Appraisal Value?

You can’t control your home’s location or square footage, but you can shape how it’s perceived. Simple updates like:

- Tightening a leaky faucet

- Touching up paint

- Replacing worn fixtures

- Giving the walls a fresh coat

Help signal that the property has been cared for. Decluttering and deep cleaning also go a long way in making rooms feel more spacious and appealing.

If you’ve made improvements, back them up with permits, receipts, or warranties. Showing that upgrades were correctly done and with documentation reassures both the appraiser and potential buyers that the home is in solid condition and worth the investment.

Do Appraisers Look Inside Closets, Basements, and Attics?

Appraisers check all accessible areas of the home they’re evaluating. That includes closets, basements, garages, and attics. They’re not there to judge your organizational skills, but they do need to verify square footage, livable space, and any signs of damage or needed repairs.

How Long Does a Home Appraisal Take, and When Will I Get the Results?

The on-site visit usually takes 30 minutes to a few hours, depending on the home’s size and condition. A newly constructed condo is quick to assess, while an older property or a fixer-upper takes more time.

Afterward, the appraiser compiles their findings into a report, which is generally delivered to the lender within about a week. The lender then shares the results with the buyer.

Are There Real Estate Transactions Without Appraisals?

In some cases, appraisals are waived or not required:

- Appraisal waivers in lending: Fannie Mae and Freddie Mac may skip the appraisal (sometimes called “value acceptance”) when borrowers have strong credit, a large down payment (20%+), and the property has plenty of sales data. Refinances with high equity may also qualify, using automated valuation models (AVMs) instead of a full appraisal.

- Cash purchases: No lender means no appraisal requirement. Buyers may still order one for peace of mind, but it’s optional.

- Special cases: VA streamline refinances (IRRRL) and some builder-financed new construction can move forward without an appraisal.

The Bottom Line: Step-by-Step Guide to Home Appraisal

A home appraisal may feel like one of the most intimidating parts of the buying or selling process, but once you understand the steps, it becomes far less overwhelming. From the moment the lender orders the appraisal to the delivery of the final report, each stage has a clear purpose: to establish a fair, data-driven value that protects both lender and borrower.

- For buyers, the appraisal ensures you’re not taking on a loan that’s bigger than the home is worth.

- For sellers, it provides validation that your asking price is realistic in today’s real estate market.

- For lenders, it reduces the risk of financing a property at an inflated value.

While many see appraisals as a hurdle, it’s a safeguard. It brings objectivity to what can often be an emotional transaction. By knowing what to expect, preparing ahead of time, and understanding your options if the number comes in higher or lower than expected, you’ll be ready to navigate this step with confidence and keep your deal moving forward.

About the Author: Preston Guyton is the founder of ez Home Search. He has been a real estate leader for over 20 years. Starting with a focus on South Carolina, he has helped coach and empower real estate professionals to achieve their full potential by meeting the needs of their local community.