Refinancing your mortgage can be a powerful financial strategy—when done at the right time. The Federal Reserve lowered its basis rate for the first time since March 2020. It is sparking hope that mortgage rates may follow suit. With lower loan rates anticipated soon, homeowners who bought in the era of higher rates are wondering if the right time to refinance is coming.

However, deciding to refinance is a matter of timing. It has to be right for your personal financial situation. Evaluate these factors to assess when refinancing your home loan is a smart move.

Understanding Mortgage Refinancing

What is Refinancing?

Refinancing replaces your original loan with a new one, often featuring different terms. This process helps homeowners secure a lower interest rate, adjust their loan terms, or access cash for other purposes.

Common Reasons for Refinancing

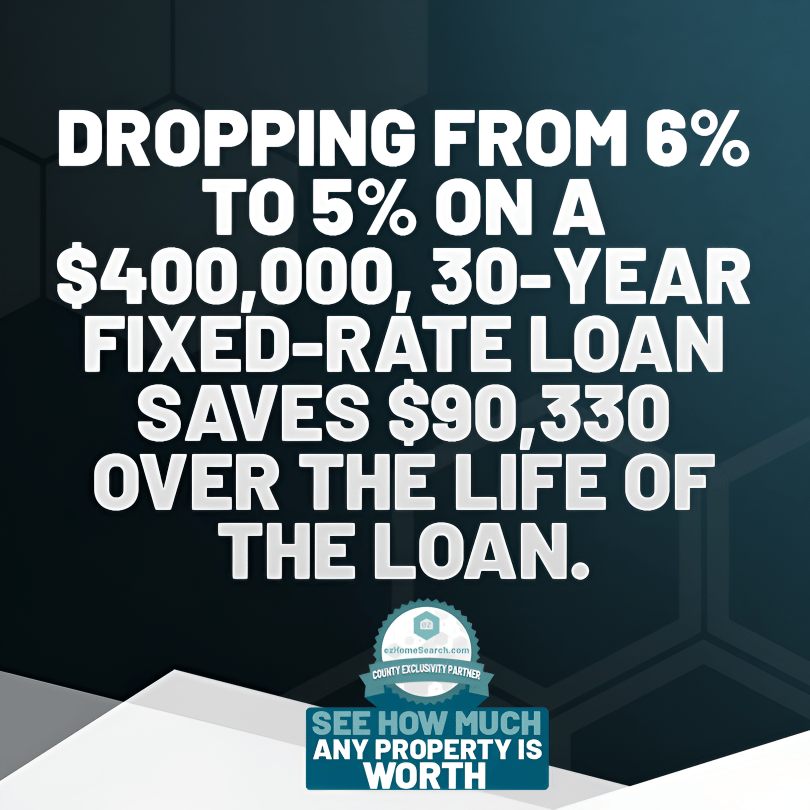

- Lowering Interest Rates: Reducing your interest rate can lead to significant savings over the life of the loan. Dropping from 6% to 5% on a $400,000, 30-year fixed-rate loan saves $90,330 over the life of the loan.

- Reducing Monthly Payments: A lower interest rate or longer loan term can decrease your mortgage payments. Using the above example, the monthly payment is reduced by $251 a month. It can also reduce payments by removing private mortgage insurance (PMI).

- Changing Loan Terms: Transition from a 30-year mortgage to a 15-year loan for a faster payoff. The same loan amount with 5% interest over 15 years will pay $169,371 in interest instead of $373,023 over 30 years.

- Change the Type of Mortgage: Homeowners may wish to stabilize their monthly mortgage payment by moving from an adjustable-rate mortgage (ARM) to a fixed-rate mortgage. They may also have enough home equity to move from a jumbo loan to a conventional loan.

- Cash-Out Refinancing: Tap into your home's equity for renovations or to consolidate debt.

Key Factors to Consider Before Refinancing

Interest Rates

Interest rates matter in refinancing decisions. The rule of thumb suggests refinancing if you can lower your initial rate by at least 1-2%.

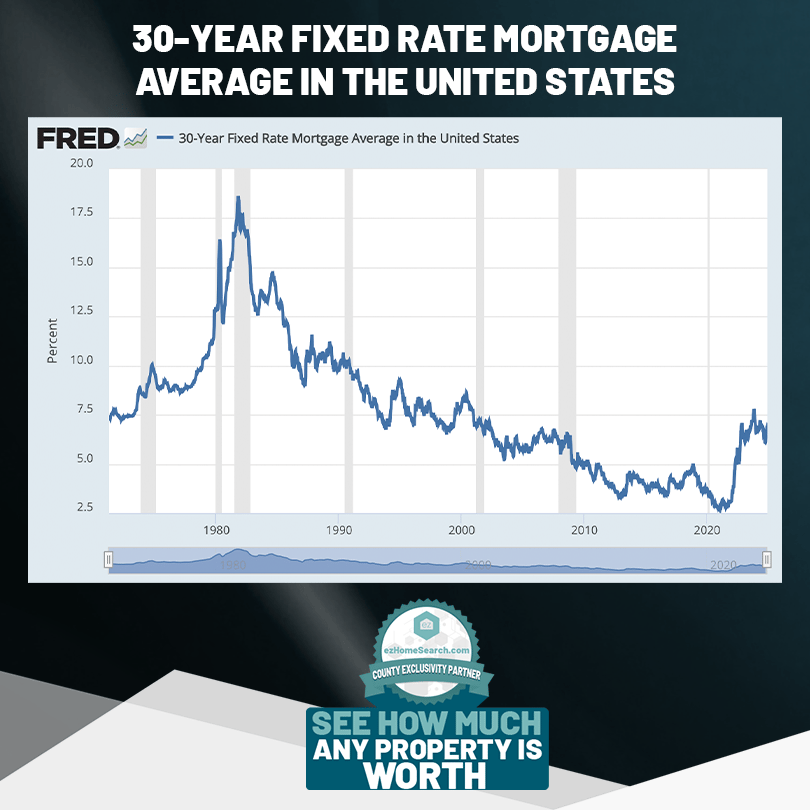

Mortgage rates fluctuate, as experienced during the pandemic. The market shifted from 2-3% to over 8% in about a year. In fall 2024, rates hovered around 6.5% for conventional mortgages and have increased in recent weeks. However, they remain over a percentage point lower than last year.

No one has a crystal ball on when exactly the mortgage rates will lower from their 6-7% range. Experts predict they will eventually stabilize around 4-5%, which is good news for those who bought at 6% and above. The best thing to do is watch the current mortgage market and be patient.

Not only does the market fluctuate, but shopping around can yield significant savings, given the varying rates offered by different lenders. Rates also vary between loan types.

Break-Even Point

What’s your break-even point? This metric tells you how long it will take to recoup the costs of refinancing. To calculate, subtract your monthly savings from your total closing costs to determine when you'll start saving money. Refinancing may be beneficial if you plan to stay in the home beyond this point.

Waiting Period

If you’ve recently bought your home, check your loan terms. Mortgage lenders often include a waiting period. This is how long you must carry the loan before it’s eligible for a mortgage refinance. Typical waiting periods are six months to one year.

Credit Score

A strong credit score is vital for securing favorable refinancing terms. If your score has improved since obtaining your original mortgage, you could qualify for better interest rates. Conversely, a drop in your credit score might make refinancing less advantageous.

Loan Term Considerations

Deciding whether to shorten or extend your loan term impacts your financial future. A 15-year mortgage may save on interest and pay off your home faster, but it increases the monthly payments. Conversely, extending to a 30-year term might lower payments but increase the total interest paid.

Closing Costs

Like your original home loan, refinancing has closing costs, which include underwriting fees, appraisal, and title insurance. These expenses affect the overall cost-effectiveness of refinancing. Run the numbers on how much the refinancing closing fee will cost and if you have those funds.

Home Equity

Typically, lenders require at least 20% equity in your home to refinance, especially if you’re considering a cash-out refinance. If your property's value has increased, you may have more options. Conversely, diminished equity might limit your refinancing possibilities. You build home equity by paying down your mortgage balance and through market appreciation.

Personal Financial Goals

Align refinancing with your long-term financial objectives. Are you aiming to pay off your mortgage early? Perhaps a shorter loan term makes sense. Do yo want to build home equity faster, or want to enhance cash flow? Do you need to make home renovations so you can age in place? Let your goals guide your refinancing decision.

When Refinancing Might Not Be a Smart Choice

Short Time Horizon

If you're planning to move soon, refinancing may not be worthwhile. The savings from reduced payments might not outweigh the closing costs and payment savings incurred. That’s why you need to calculate the break-even point.

Rising Interest Rates

In an economic environment where rates are climbing, locking in a lower rate may not be possible. Assess market trends and projections before making a decision. Keep track of current interest rates as compared to your current loan.

Unfavorable Credit Situation

Poor credit can lead to higher rates and less favorable terms. Keep your credit in good standing before pursuing this option. Work on improving it before refinancing.

Risk of Extending Debt

Extending your loan term can lower monthly payments but increase the total interest paid over time. Consider your financial strategy before making this trade-off.

Best Scenarios for Refinancing

When Interest Rates Drop Significantly

Refinancing is most beneficial when current rates are substantially lower than your current home loan rate. Even a 1% reduction can lead to significant savings. Watch the 10-Year Treasury Yield for a better sense of where the mortgage market may go in the months ahead.

When Your Credit Score Has Improved

Improved credit can result in better loan terms, making refinancing advantageous. You are entitled to one free credit report each year. Check your credit score and compare available rates from multiple lenders.

Switching from an Adjustable-Rate Mortgage (ARM) to a Fixed-Rate Mortgage

Converting an ARM to a fixed-rate mortgage provides stability and predictability in your monthly payments. This type of refinance is a rate-and-term refinance.

When You Want to Cash Out Equity

Accessing your home's equity through refinancing can provide funds for home improvements or consolidate high-interest debt. A cash-out refinance may align with your broader financial goals.

To Shorten the Loan Term

Accelerating your mortgage repayment term can reduce what you pay in interest, building home equity faster. And, as you’ll pay off earlier, it may free up funds for other investments.

Steps to Take Before Refinancing

Evaluate Your Financial Situation

Assess your current budget, credit score, and long-term goals. This analysis will help you determine if refinancing aligns with your financial plans. Use online calculators or consult a financial advisor to understand the long-term impact of refinancing. Factor in all associated costs and potential savings.

You may also wish to check your home equity through an estimator or a home appraisal. Owning at least 20% of your home’s value helps waive private mortgage insurance or qualify you for a conventional mortgage. It can also help secure better refinance rates.

Shop Around for Lenders

Compare rates, terms, and closing costs from multiple lenders to ensure you get the best deal. Refinance programs can vary across the market. Don't hesitate to negotiate for more favorable loan conditions.

Get Pre-Approved

Understand what you qualify for before making a decision. Pre-approval clarifies the mortgage terms you can expect and strengthens your negotiating position.

Let a Refinance Help You

Refinancing your home can be a strategic financial move, but do evaluate the benefits and drawbacks carefully. Make informed decisions that align with your long-term goals. Refinancing doesn’t make sense in every situation. Given that current market indicators hint that interest rates are poised to decline in the months ahead, refinancing will likely become more popular among homeowners. Remember, consult with professionals who can help you navigate refinancing a mortgage.

About the Author: Preston Guyton is the founder of ez Home Search. He has been a real estate leader for over 20 years. Starting with a focus in South Carolina, he has helped coach and empower real estate professionals to achieve their full potential by meeting the needs of their local community.